The Errant Benefit of Hindsight

I love the "Missing out on the best days in the market can be costly" marketing pieces. Investment companies fire them off every single time there's a bit of market volatility (like right now).

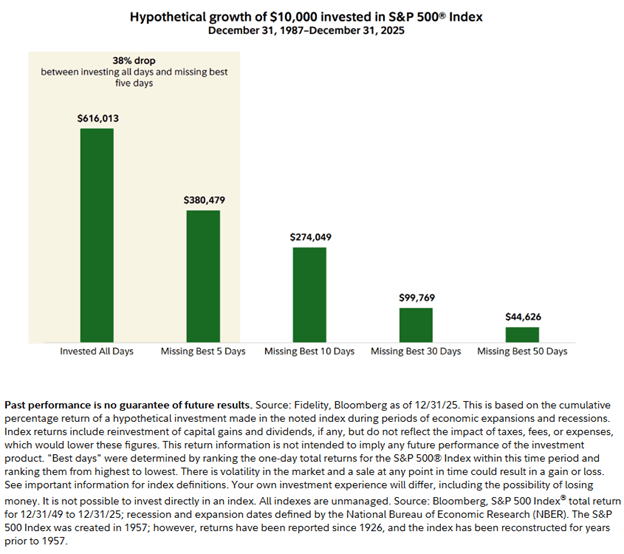

Here's one from Fidelity Investments.

If you've read most of what I've written, you'll know I love this kind of content. "Stay invested no matter what," "just keep buying," "buy now, sell never."

Successful investing means you must endure and live through market volatility. Both good volatility and bad. You don't get one without the other.

Some people in the investment profession hate this kind of content, though. They say context matters and it does, so let's address the reasons they call it "the myth of missing the best days."

The best days happen during the worst markets.

This is true. They nailed this part: good days and bad days cluster during heightened market volatility.

But that's the point. Good financial professionals will remind you, always to the point of annoyance, that to earn long-term stock market returns, you must subject yourself to horrific markets.

Volatility is mathematically devastating.

I like the point they make here.

When your investments drop 25%, you don't need to then earn 25% to breakeven. You need to earn 33%.

Here's the math: $10,000 falls to $7,500. To earn $2,500, your now $7,500 needs to earn 33% to get back to $10,000.

When they drop by 33%. You need to earn 50%.

Drop by 50%. You need to earn 100%.

I'm sure you get it by now, and I'll come back to how they have it backwards.

They then link that "devastating math" to sequence of returns risk (SoRR). I've written about SoRR here and here.

To avoid SoRR set aside a war chest not considered part of your retirement assets and use a dynamic withdrawal strategy.

How they have it backwards.

The math they use to scare you works in reverse.

Let's use the 33% drop as an example. And remember, we're never going to sell our investments. If we need retirement income during a crash, we'll use the war chest.

The average recovery to new all-time highs after a market crash has taken just over two years, but let's use three just to be safe. Your compounded** returns would be almost 14.5%/year.

If it took four years, you'd earn close to 11%/year. And about 8.5% if it took five years.

Those are powerful returns. And, as history tells us — even if it isn't indicative of the future*** — good markets last a lot longer than bad ones.

What about missing the worst days?

I'll use their data for this part, even though it isn't clear exactly what index they've used. You can go to their site to see it. It's linked above.

To them, missing the ten worst months between 1988 and 2023 "is more than three times as powerful as staying in the market via buy and hold and capturing the best periods."

If only it were that easy. We only know the worst months in the market with hindsight. It's a history lesson. We humans in the present have no idea — none! — if this month will be the worst, or the next one, or the one after that.

Here’s how they conclude:

"If there's one thing the last 30 years of data screams loudest, it's this: An investor's long-term success, especially near or in retirement, depends more on avoiding deep drawdowns than on obsessing over capturing the best days in the market." The italics are theirs.

Exactly. But find me a method that allows an investor to avoid only the worst days and months in the market. You can't. Because all you have is history.

*Sell when you need income in retirement, of course. I'm sure you get my point.

**Money grows on top of money, so the math isn't as straightforward as they make it out to be.

Raymond James Ltd. is a Member Canadian Investor Protection Fund. Information in this article is from sources believed to be reliable; however, we cannot represent that it is accurate or complete. It is provided as a general source of information and should not be considered personal investment advice or solicitation to buy or sell securities. Data in these charts is from sources believed to be reliable, but accuracy cannot be guaranteed. This provides links to other Internet sites for the convenience of users. Raymond James Ltd. is not responsible for the availability or content of these external sites, nor does Raymond James Ltd endorse, warrant or guarantee the products, services or information described or offered at these other Internet sites. Users cannot assume that the external sites will abide by the same Privacy Policy which Raymond James Ltd adheres to.

Raymond James (USA) Ltd. (RJLU) advisors may only conduct business with residents of the states and/or jurisdictions for which they are properly registered. Raymond James (USA) Ltd., member FINRA/SIPC