SoRR Redux

I share this post about Sequence of Returns of Risk (SoRR) more than any other.

That’s because I believe planning for a market crash early in retirement is vital. I’m a bit biased about this because when I started my career in 2010, I met tons of investors who had been allocated entirely to equities or equity-funds when they retired in 2007. To fulfill their retirement income needs they needed to sell heavily discounted investments, and doing so put them at risk of running out of money later in retirement. I was the guy in his early 20s saying to retirees, “Hey, you should consider getting a part-time job otherwise you’re going to run out of money.” Those were not comfortable conversations.

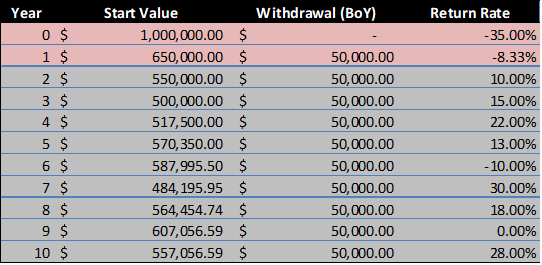

Here’s what I mean with numbers that aren’t anywhere near as bad as 2007 or 2008.

*BoY indicates a withdrawal at the beginning of the year.

**Reverse the sequence (best years first, worst years last) and the same portfolio ends at roughly $1.35M. Nearly $800,000 more, with nothing changed but the order.

Look how quickly your investment account could deteriorate with bad timing and without making adjustments. After ten years of 50K withdrawals and a brutal start, you’ve got 557K left from a million. And you’ve been lucky since year two.

And I know those numbers are unrealistic, but the dynamic isn’t. Just imagine for a minute that you retired with a million dollars, and then a year later it was worth 650K. You’d think, “It’ll be OK. Markets recover,” and take out your 50K. Then a year later it’s even worse. You’re checking your portfolio daily. Your friends and family are telling you what they’ve done and what’s worked for them. You’re now subscribed to all the investing YouTube channels. You’re even commenting on the posts. You start doubting yourself.

And then these thoughts start keeping you up at night.

It will get worse.

“My million-dollar portfolio is now worth half a million. That’s ten years of growth down the drain. At 50K a year, I’ve got ten years of spending left. I might as well roll everything into GICs. At least I’ll be able to squeeze out an extra year or two.”

If only I had [enter strategy you’re thinking of now with the benefit hindsight].

“If only I had retired two years later. If only I had saved more earlier. If only I had put all my money into GICs when I retired. If only….”

I can invest my way out of this.

“That stock looks beaten up. The YouTubers like it. If it gets back to where it was trading five years ago my money could quintuple! That would fix this. I’m going to do it.”

Dramatic, I know. But those thoughts are exactly how investments mess with your brain. You basked in decades of growth before this untimely crash. Your investments may well have doubled two or three (maybe even four times) while you were accumulating this nest egg. You left all those people who were too scared to invest, who earned GIC returns for their entire lives and whose money never doubled, in the dust. But now they look like geniuses. They aren’t going to run out of money. But you might.

It’s fine to have those thoughts. Everyone does. You just can’t act on them.

So what do you do about it?

I covered this in detail in the original post linked at the start of this post, but here's the short version.

First, build an emergency fund (we call it a war chest) outside your retirement nest egg. Enough to cover two to five years of income needs. I suggest two. Keep it completely separate from your investments.

If the market crashes early in retirement, you draw from the war chest instead of your investments. You won’t be forced to sell at the worst possible moment.

Second, use a dynamic withdrawal strategy (link here). If your portfolio drops far enough that your withdrawal rate becomes unsustainable, you take a pay cut. If markets recover and your portfolio grows, you give yourself a raise. It sounds simple because it is. But it requires a plan you trust before the bad times arrive. Because you probably won't think clearly after a 35% drop.